How to Open a European Business Account for UAE Company in 2026

Trade routes are shifting and some banks are quietly closing doors to the region. Here’s how UAE businesses can secure a European business account in 2026.

Opening a European business account for UAE company is now more accessible than ever — and in 2026, it can be done entirely online. If your business is registered in the UAE and you work with European clients, pay European suppliers, or need a SEPA & SWIFT-capable IBAN to keep payments flowing, this guide walks you through every step: why you need it, what’s changed, the exact documents required, and how to open your account fully remotely.

| ✦ Transferra is open for UAE businesses — right now The past months haven’t been easy for UAE businesses. Trade routes are shifting, some banks are quietly closing doors to the region, and there’s a general feeling of: “Will my next payment actually go through?” Transferra is onboarding UAE clients right now – fully remotely, no office visits needed. Your account runs through UK and European banking infrastructure, so regional disruptions don’t touch your payment flows. Most transfers still arrive the same day. |

Why a European Business Account for UAE Company Is Essential in 2026?

The UAE is one of the world’s leading business hubs — but when your clients are in Germany, your suppliers are in Italy, and your SaaS subscriptions bill in euros, a UAE dirham account creates friction at every step. Here’s what a European account actually solves:

- SEPA access — send and receive payments within 36 European countries instantly and at near-zero cost

- EUR invoicing — issue professional euro invoices with a local IBAN that European clients trust

- Lower FX costs — hold EUR balances and convert only when rates suit you, rather than converting every incoming payment

- Partner trust — European businesses and banks feel more comfortable transacting with an EU or UK IBAN

- Payment continuity — insulate your payment flows from regional banking volatility

- Faster settlements — SEPA Instant transfers arrive in seconds; SWIFT from UAE can take 1–3 business days

| The grey list is history — but due diligence remains In early 2024, the UAE was officially removed from the FATF grey list. This was a significant milestone: European banks and EMIs can now work with UAE companies without the heightened automatic scrutiny that came with grey-list status. That said, compliance checks are still thorough. UAE companies are not treated identically to EU-registered businesses — but the door is now genuinely open. |

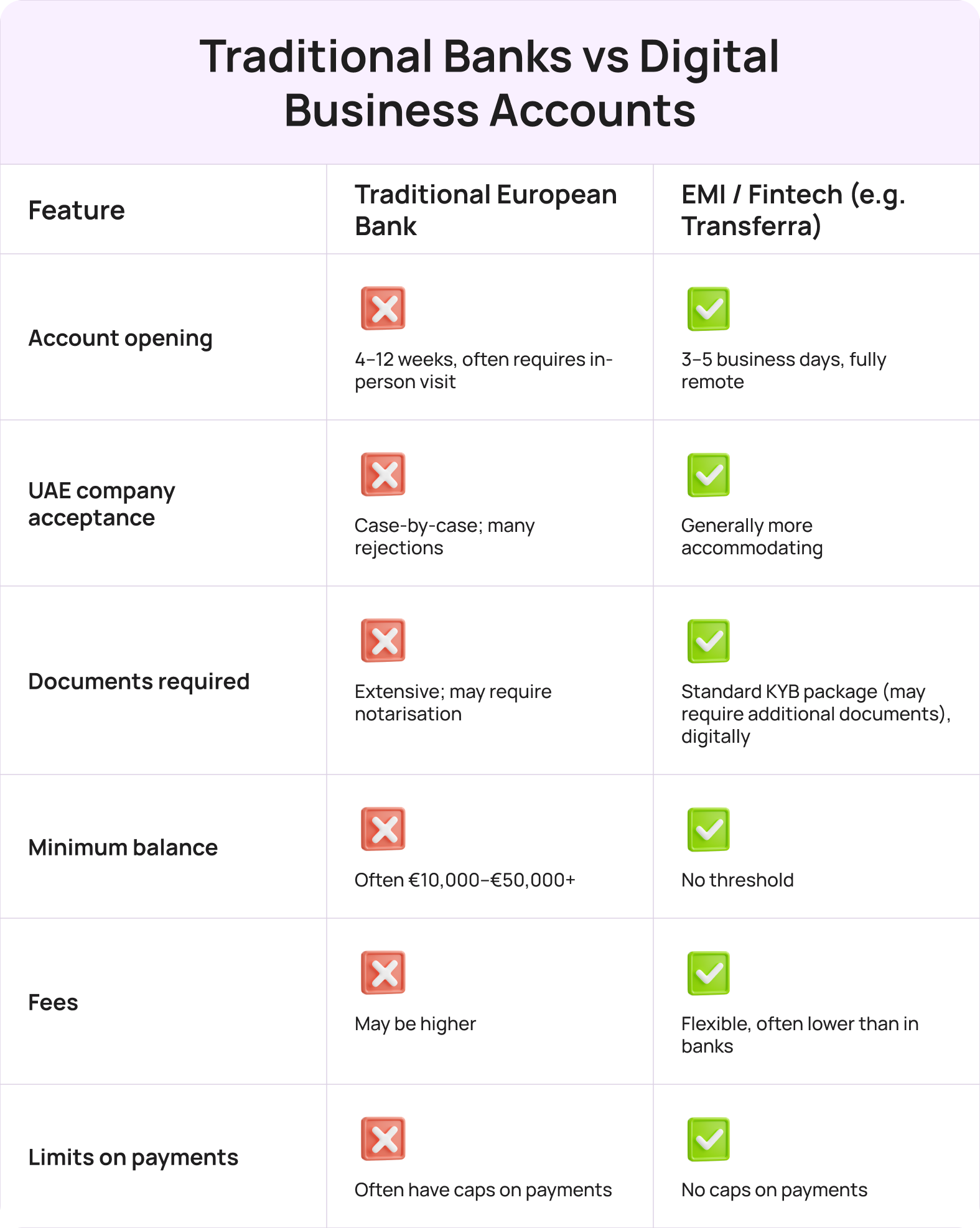

Traditional European Bank vs. EMI: Which Route Is Right for You?

When choosing a European business account for UAE company, the choice between a traditional bank and an EMI is the most important decision you’ll make.

For most UAE companies that need reliable European banking without months of waiting or flights to Frankfurt, an FCA-regulated EMI with a European IBAN is the practical choice in 2025.

Step-by-Step: How to Open a European Business Account as a UAE Company

Step 1 — Choose your provider

The first step to opening a European business account for UAE company is choosing the right type of provider. Decide between a traditional bank and an EMI. If speed, remote onboarding, and flexibility matter, an FCA-regulated EMI is almost always the faster path for UAE-based companies. Look for: SEPA + SWIFT support, multi-currency wallets, a dedicated manager, and clear fee structures.

Step 2 — Check your eligibility

Most EMIs and banks will want to understand your company structure before you even start. Common eligibility factors:

- Company registered in the UAE (mainland, free zone such as DMCC, DIFC, IFZA, RAKEZ, SHAMS, ADGM — or offshore)

- Clear and legitimate business activity — trade, IT, consulting, logistics, e-commerce, professional services

- No sanctions exposure on shareholders, directors, or UBOs

- Source of funds that can be explained and documented

- No requirements to be a UAE resident — non-resident directors are accepted by most EMIs

| Free zone or mainland — does it matter? Free zone companies (DMCC, DIFC, IFZA, RAKEZ, etc.) are widely accepted by EMIs and UK-regulated institutions. Offshore UAE entities face somewhat higher scrutiny — not because they are inherently problematic, but because the activity and client base need to be clearly documented. Mainland companies generally have the strongest approval profile. |

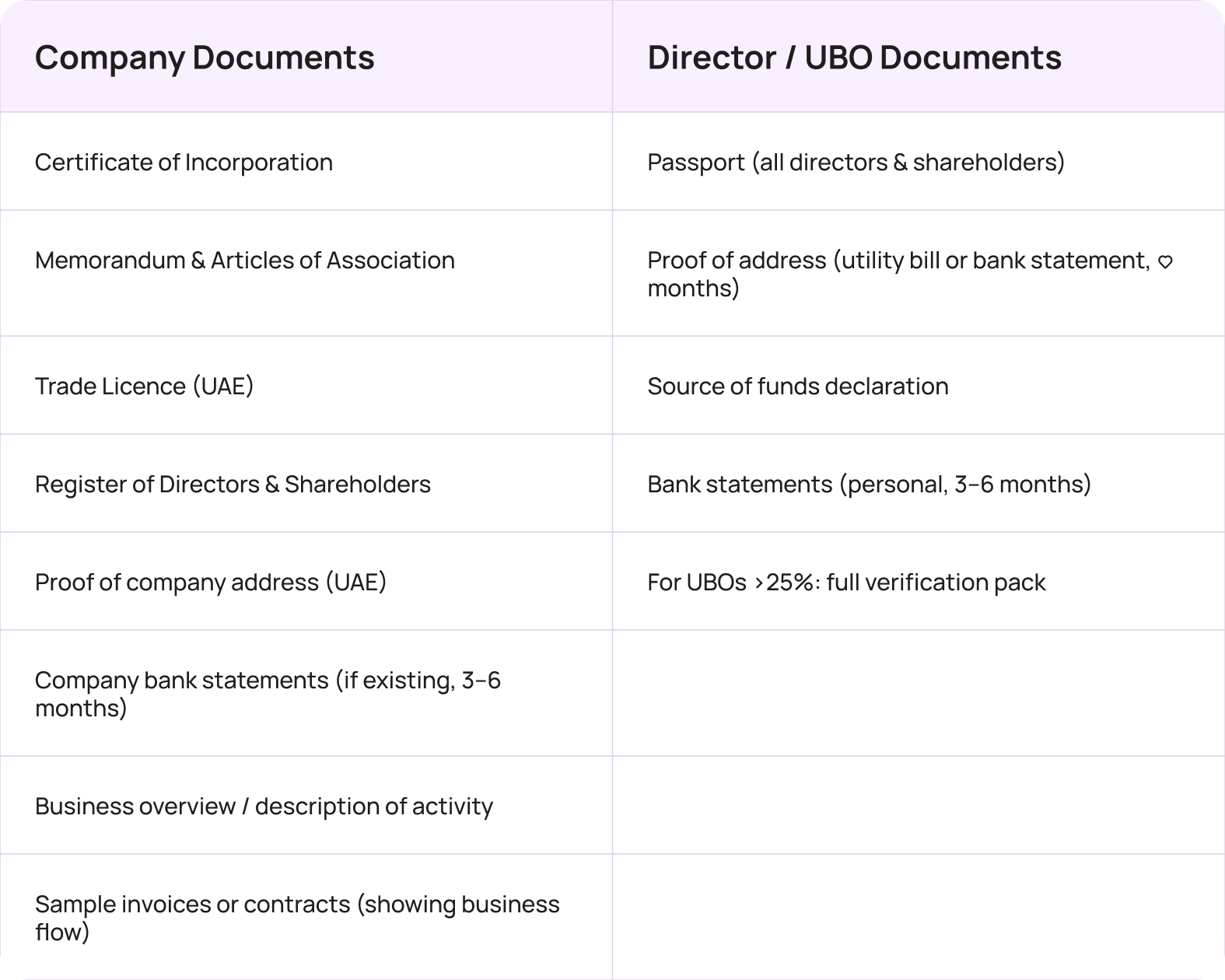

Step 3 — Prepare your documents

Get these ready before you apply. Having a complete package from the start is the single biggest factor in approval speed:

Pro tip: All documents must be consistent — the same company name spelling, same director names, matching addresses. Discrepancies are the most common reason for delays.

Step 4 — Submit your application

With an EMI like Transferra, the process is fully digital:

- Register online and create your business profile

- Upload your company and personal documents via the secure portal

- Complete the KYB (Know Your Business) questionnaire — business activity, expected volumes, payment flows

- Your dedicated manager reviews the application and contacts you if anything is needed

- Compliance team completes AML/KYC checks

- Account approved — typically within 3 business days for straightforward applications

Step 5 — Verification and KYC

Unlike traditional banks, which often require in-person interviews, most EMIs complete verification remotely. This typically involves:

- Identity verification via video call or biometric ID scan

- Confirmation of business activity and payment flow

- Source of funds review — particularly important for UAE companies with significant turnover

With Transferra: no office visits required. The entire process happens online, with a dedicated manager available to guide you through every step.

Step 6 — Account activation

Once approved, you receive your account details including your European IBAN. You can immediately start sending and receiving payments in EUR, GBP, USD, and 40+ additional currencies. SEPA and SWIFT are both available from day one.

Opening a European Business Account for UAE Company with Transferra: What UAE Businesses Get

| ✦ Transferra is open for UAE businesses — right now The past months have been turbulent for UAE businesses dealing with European payments. Some banks are stepping back. Correspondent banking relationships are shifting. Payment routes that worked last year are being quietly discontinued. Transferra has not stepped back. Onboarding UAE clients right now — fully remotely, no travel requiredUK-regulated EMI (FCA authorised) — your funds are safeguarded under UK Electronic Money RegulationsUK and European banking infrastructure — regional volatility in the UAE doesn’t affect your payment railsMost transfers arrive the same business dayDedicated account manager from day one — a real person who knows your business, not a support ticket queue40+ currencies, SWIFT, SEPA, SEPA Instant, Faster Payments — all on one account |

- Hold and transact in 40+ currencies under a single IBAN

- SEPA and SEPA Instant for European payments

- SWIFT for international transfers to 230+ countries

- Unlimited Visa virtual debit cards — Apple Pay and Google Pay enabled

- Competitive FX rates with no hidden conversion markups

- Multi-user access with granular permissions — suitable for teams

- ISO 27001 certified — enterprise-grade data security

Common Mistakes UAE Companies Make (and How to Avoid Them)

| Mistake 1: Submitting incomplete documents A missing UBO declaration, an expired trade licence, or a company address on file that doesn’t match the incorporation certificate will stop your application immediately. Prepare everything before you submit. |

| Mistake 2: Applying to a traditional European bank without preparation Traditional banks are significantly stricter with non-EU companies and often reject UAE applications outright — especially for free zone or offshore entities, or businesses in industries they consider higher risk (trading, digital services, crypto). An EMI is almost always a faster, more reliable first step. |

| Mistake 3: Underestimating the importance of business narrative Compliance teams don’t just look at documents — they look at whether your business makes sense. A clear, concise description of: what your company does, who your clients are, where your income comes from, and why you need a European account dramatically improves approval rates. |

| Mistake 4: Applying to multiple providers simultaneously without a strategy Multiple rejections create a compliance paper trail that future providers can see. Apply to your best-fit provider first with a complete, well-prepared package, rather than shotgunning applications across ten banks. |

Frequently Asked Questions

Below are the most common questions we hear from businesses researching how to open a European business account for UAE company.

Can a UAE free zone company open a European business account?

Yes. Companies registered in major UAE free zones — DMCC, DIFC, IFZA, RAKEZ, SHAMS, ADGM, and others — can open European business accounts with EMIs. Free zone entities are widely accepted, provided the business activity is clear and documents are in order. Traditional European banks may be more restrictive.

Do I need to travel to Europe to open the account?

No — not with an EMI. UK-regulated providers like Transferra complete the entire onboarding process remotely. Document upload, identity verification, and KYB can all be done online. Traditional European banks may still require in-person visits for UAE-based applicants.

How long does it take?

With an EMI: typically 3–5 business days for a complete, straightforward application. Complex structures (multiple shareholders, holding companies, higher-risk industries) may take longer. Traditional banks can take 4–12 weeks.

Will a UAE company be automatically flagged as high risk?

No longer automatically. The UAE’s removal from the FATF grey list in early 2024 changed this. That said, UAE companies still undergo thorough compliance checks. Clear documentation, a well-explained business model, and a clean beneficial ownership structure significantly improve approval odds.

What currencies will my European account support?

With Transferra: 40+ currencies including EUR, GBP, USD, AED, CHF, CAD, AUD, and many more — all accessible from a single account. You can hold balances, send, receive, and convert between currencies as needed.

Can I use the account for high-value transactions?

Yes. Transferra is designed for business-grade transaction volumes. There are no arbitrary low limits — account capacity is aligned with your declared business profile. High-value transfers are supported via SWIFT and SEPA without restrictions beyond standard compliance checks.

What happens to my payments if there are regional banking disruptions?

With Transferra, your account runs through UK and European banking infrastructure. Disruptions to regional payment networks or correspondent banking relationships in the UAE do not affect your Transferra payment flows — your SEPA and SWIFT access remains stable regardless of what’s happening on the ground.

Ready to Open Your European Account?

The path of opening european business account for UAE company is shorter than most business owners expect — provided you go in prepared and choose the right provider.

For UAE businesses that need speed, reliability, and a provider that actually understands the region: Transferra is onboarding UAE clients right now. Fully remotely. With a dedicated manager at every step.

Open your account at transferra.uk — or get in touch to discuss your specific structure before applying.